The LPPT Case for Transforming Tax Administrations in Nigeria

This tax administration note was developed following the Nigeria Governors’ Forum’s (NGF) March 2024 Virtual Learning Series (VLS) for State IRS leaders which focused on sharing peer experiences on Professionalising State Revenue Administration in Nigeria.

Rising Citizen Demands are Putting Pressures on Government Revenues

With government revenues increasingly encumbered by high debt levels and rising expenditure commitments, the Nigerian economy could be facing a repeat of the 2015 economic crisis. There are fiscal imperatives and civil pressures for the federal and sub-national governments to grow their revenue base to meet the growing expectations of citizens. Equipped with more information and access to public finance data than any previous time in history, citizens are demanding that governments be more efficient in delivering services and, more importantly, transparent in how these services are delivered. These expectations are founded on the principle of the social contract – a reciprocal relationship where citizens exchange their right to self-government in exchange for the delivery of essential services and protection.

In exchange for the services citizens expect, governments need to generate revenue, and the primary instrument for revenue generation is taxation.

Uneven Progress Across States

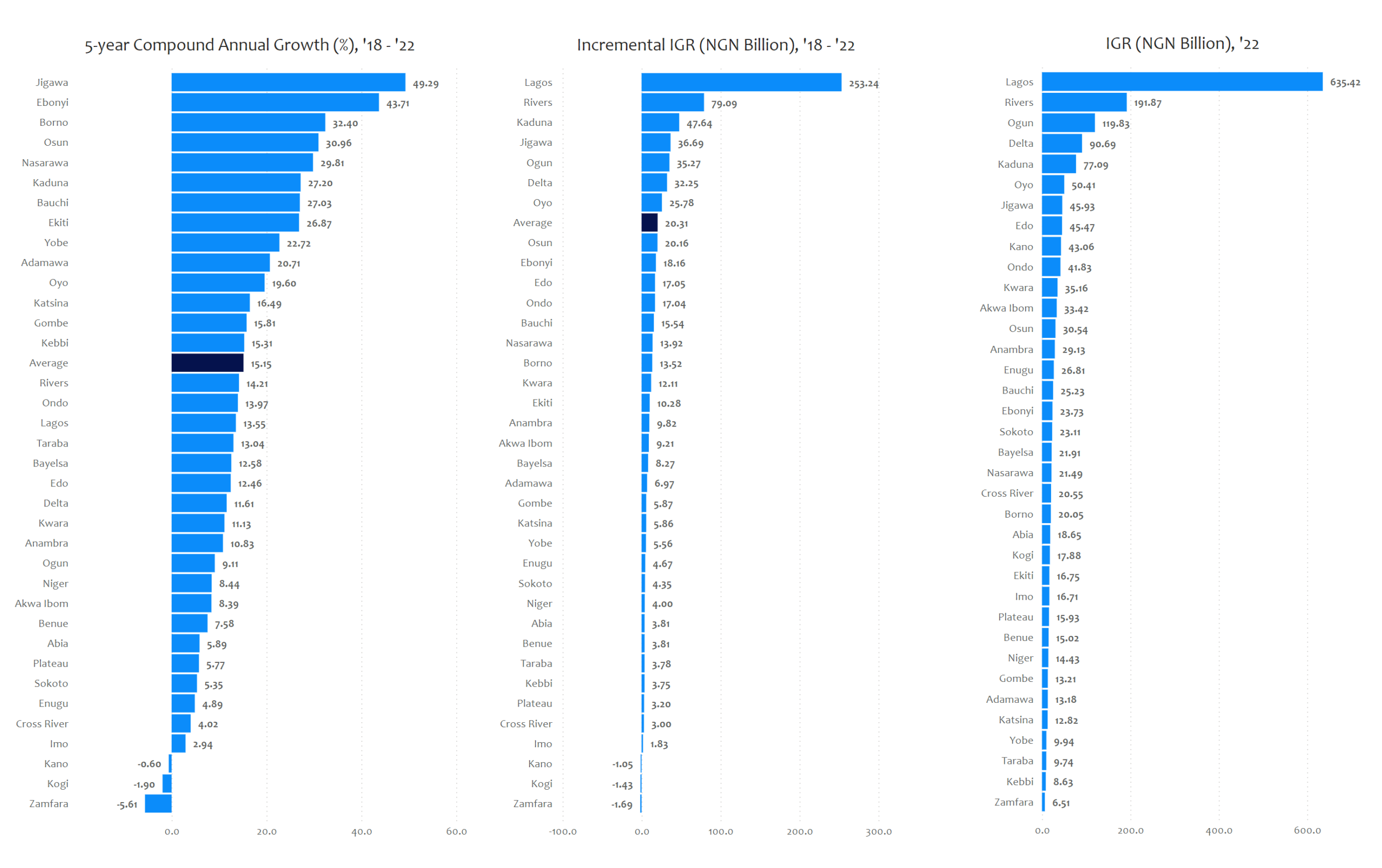

Revenue mobilisation at Nigeria’s sub-national level is recording an uneven level of transformation. Data suggests that the tax reforms and revenue growth recorded have been accounted for by only a few States. In the last five years (2018 – 2022), the 36 State governments generated a collective N731 billion in internally generated revenue (IGR), averaging N146 billion annually. Over the period, the IGR of States grew from N1.1 trillion to N1.84 trillion. Lagos State was the top contributor, accounting for 30% of the incremental revenue with N253 billion. Rivers, Kaduna, Jigawa and Ogun followed with incremental revenues of N79 billion, N47.6 billion, N36.7 billion and N35 billion, respectively. These figures include all taxes, fines, fees, levies, and charges collected by the State ministries, departments, and agencies (MDAs) during the period.

Paradoxically, only five States – Bauchi, Kaduna, Lagos, Nasarawa, and Osun – achieved yearly positive IGR growth throughout the period.

Source: Computed based on data from the 2022 Audited Financial Statements of States

Transforming Tax Authorities in Nigeria: The Law-People-Process-Technology (LPPT) pathway

To ensure that State governments can raise enough revenue to match their revenue potential, it is necessary to establish functional tax authorities that will be responsible for collecting taxes and other forms of government income on their behalf. This transition for tax authorities to become ‘functional’ hinges on four key factors that will help them move away from operating as traditional bureaucratic structures to more efficient and data-driven authorities – including a legal framework that gives them administrative and financial autonomy, a change management process that will ensure that they are able to implement incremental reforms like attracting and retaining skilled staff through competitive hiring processes and professional development, business process transformation, and technological innovation.

States that have seen their revenue base grow have generally followed this pathway. States like Lagos, Kwara and Ondo provide key lessons that have worked, demonstrating successes from the implementation of the law-people-process-technology (LPPT) pathway.

Kwara State’s success story demonstrates the transformative power of fiscal and administrative autonomy in tax administration. In 2015, the State granted its revenue service (KWIRS) the independence to hire skilled staff through a competitive process, retain or dismiss staff as necessary and manage its own budget. This autonomy, backed by a supportive legal framework, saw Kwara improve its IGR ranking from 30th to 11th place nationally, and 1st in its geopolitical zone.

Incremental change management and business transformation is feasible once a legal-institutional framework has been established. Ondo State’s Internal Revenue Service (ODIRS) demonstrates this principle in its journey to ensure its businesses are fit for purpose, efficient and dynamic. One of the areas where this is apparent is in human capital management. The State’s first step was a peer review visit to the IRS of Lagos and Kwara to learn and establish good practices that had worked in the two States. During Ondo State’s transition, its old revenue building was notably demolished, and a new one constructed to represent a new regime and signal a psychological break from the old practice.

The fourth pillar, which reinforces the change management process, is the introduction of innovation and technology to transform business processes and increase operational efficiency. The Lagos Internal Revenue Service (LIRS), Nigeria’s highest-performing sub-national tax authority, is at the forefront of the introduction of automation to streamline processes like tax filing and payments. Their e-tax system is significantly reducing compliance costs and offering digital payment solutions to taxpayers living in Nigeria’s main economic hub.

The Call to Action for Governments and Citizens

Evidence shows that this transition for any State must begin with a clear understanding and appreciation by the State Governor that independence is critical to the success of any high-performing tax administration. Without strong political will and freedom from undue influence, tax authorities struggle to enforce established tax rules even with a legal framework in place. Besides its importance during the transitional stage, independent tax authorities are less susceptible to political pressure to lower taxes or grant exemptions to favoured groups. This is often the difference between high-performing States and those without significant revenue growth.

Poor stakeholder engagement has also proved to be a major challenge for many States. Labour, civil society, professional bodies and other MDAs can be powerful allies in promoting change, but failing to involve them can stall progress. This is why understanding the stakeholder environment is essential. The contrasting experiences of Kwara and Ondo States offer valuable lessons – while KWIRS took a bold approach and implemented a full-scale change in its personnel with rapid results, ODIRS took a more measured approach, by retaining existing staff who agreed to meet new performance standards. This concession allowed ODIRS to retain institutional memory while setting new practices in human capital management and a culture of professionalism.

Benchmarking and peer learning can provide valuable information for States to build an adaptable template for this tax transformation journey.

Finally, political interference and corruption remain core watch points. Weak oversight and lack of autonomy create fertile grounds for bad policy and administrative choices. Citizens can play a greater role in pushing for tax transparency by ensuring that all revenues collected by tax authorities and State governments are accounted for and contribute to public good.

Written by David Nabena, Chief Economist, Nigeria Governors’ Forum, Abuja.